Bayesian Inference:

What is the posterior and why should I care?

Data Philly, Feb. 2024

Dante Gates

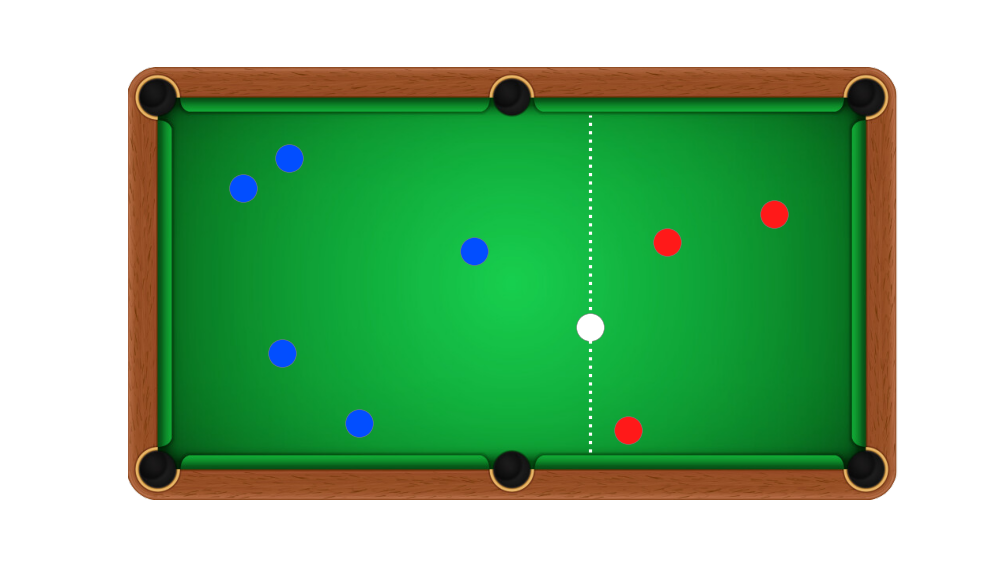

Premise

- An initial ball is rolled (colored white)

- Subsequent rolls that fall to the left, score for Alice (colored blue)

- Rolls that fall to the right score for Bob (colored red)

- First player to reach 6 points wins

The problem

Alice has scored 5 times, Bob has scored 3, what was the position of the first roll?

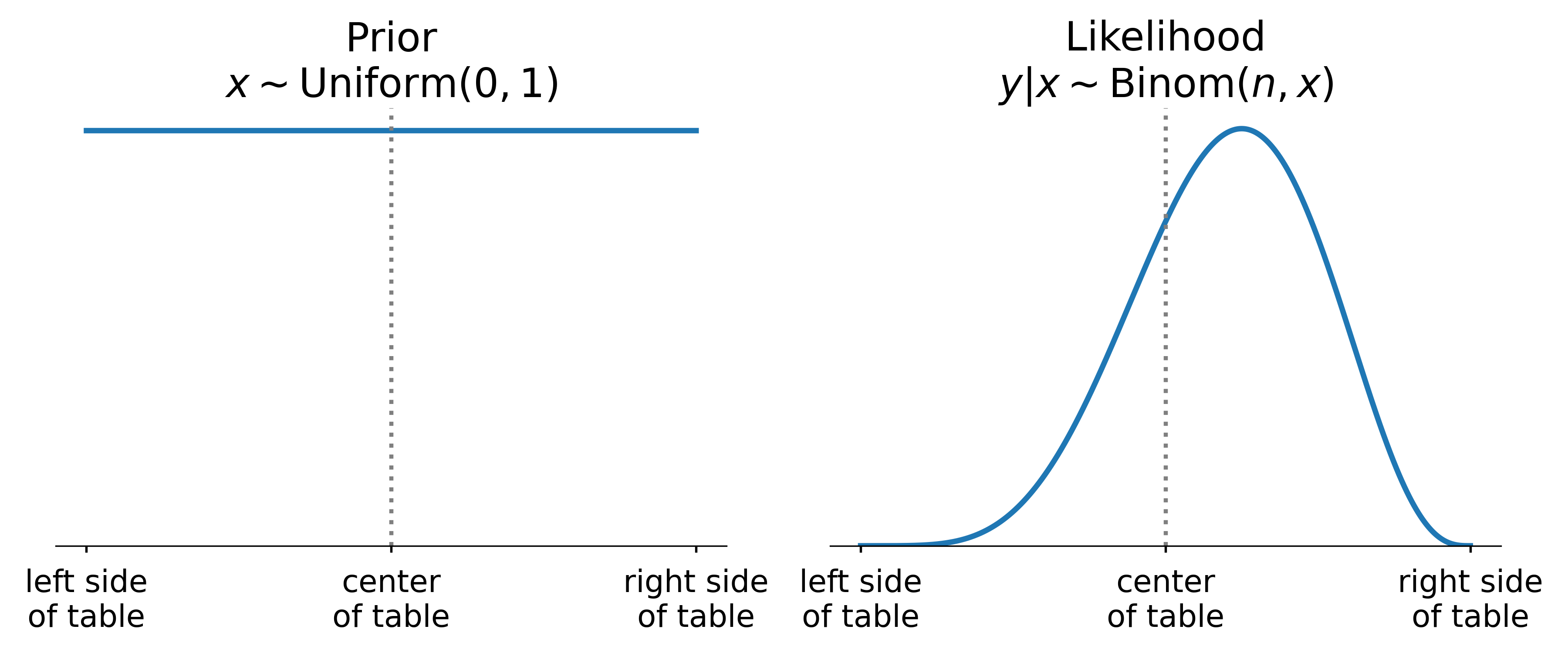

Model likelihood: P(y\vert D)

Model priors and likelihood

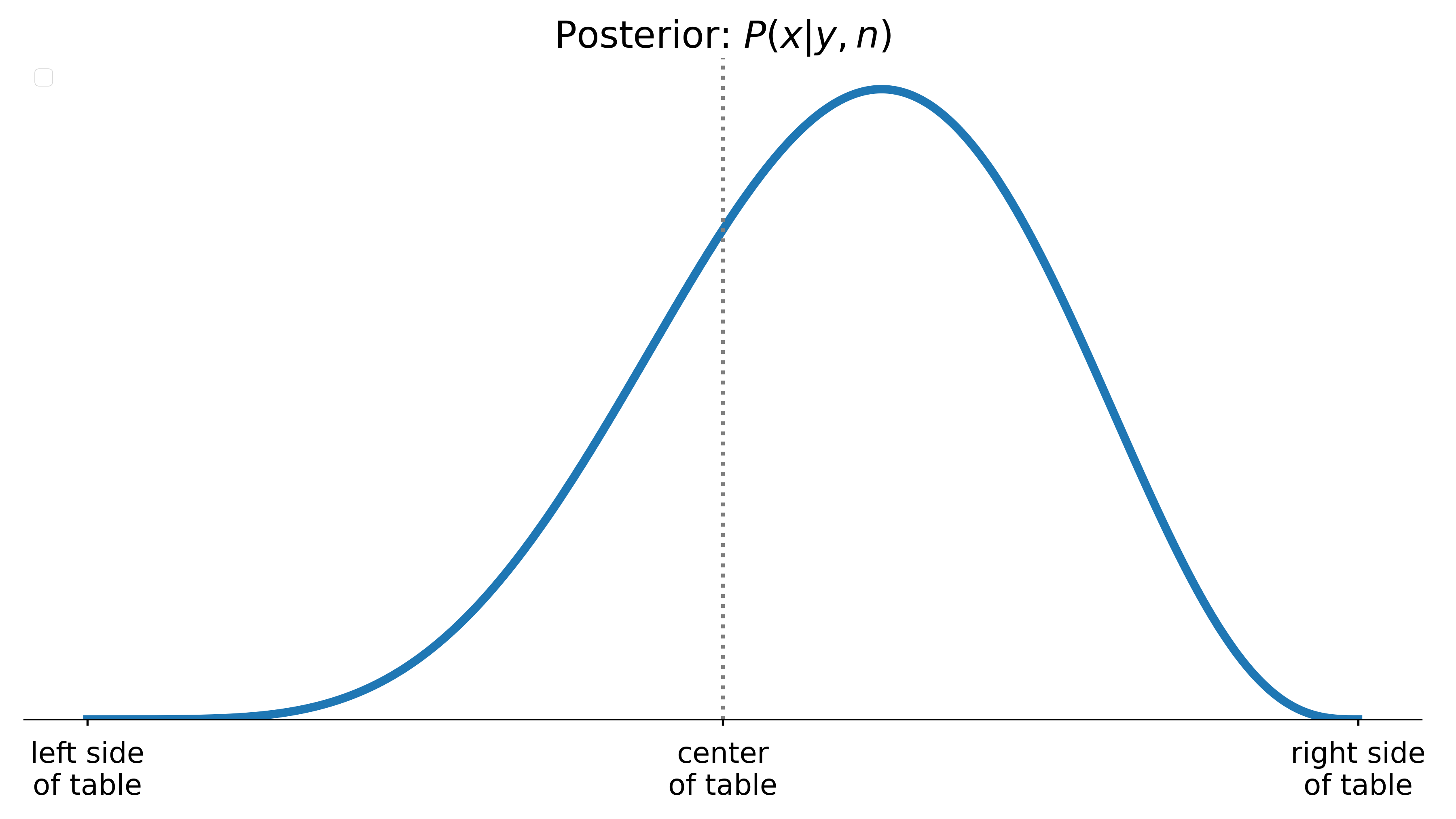

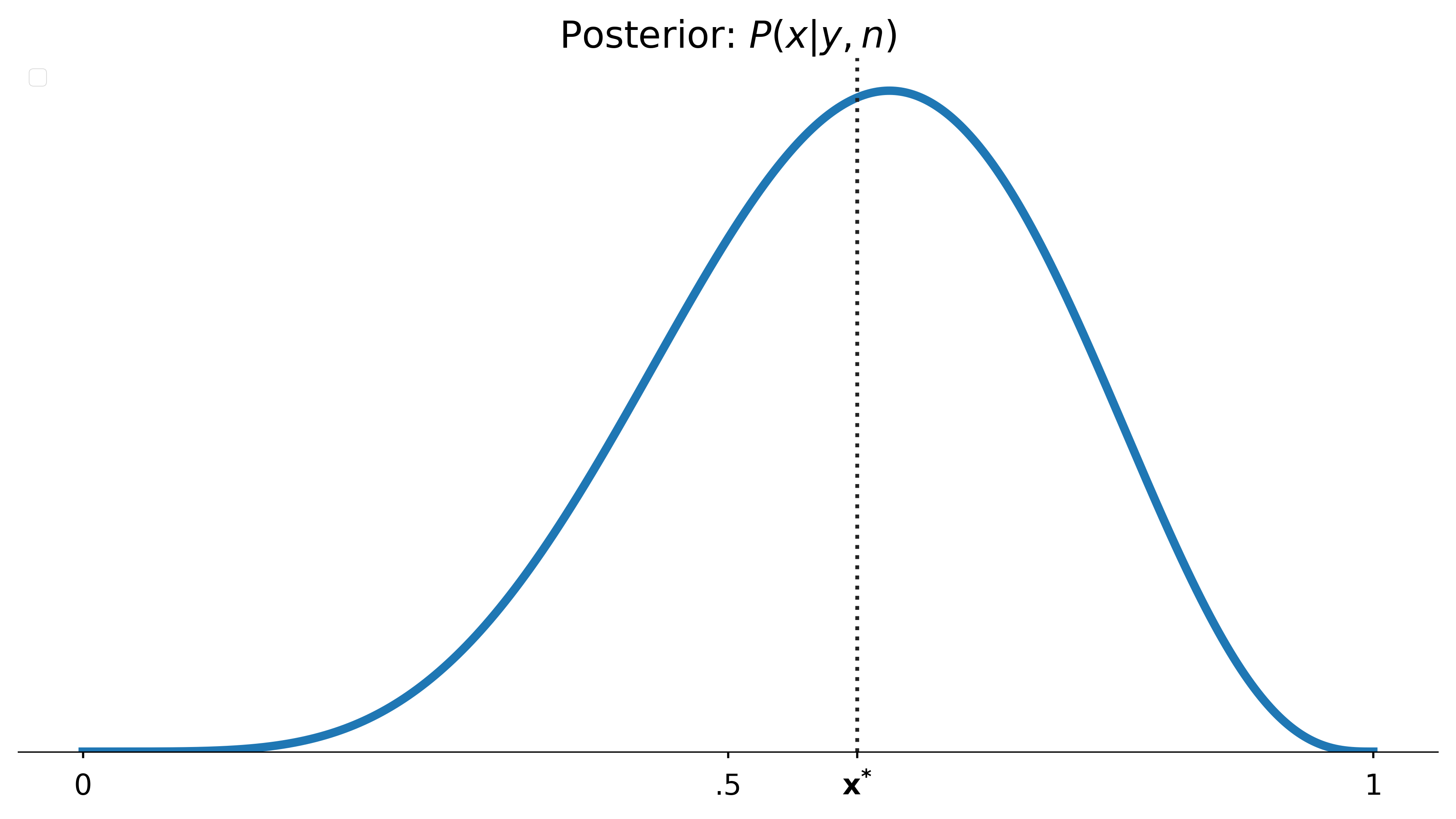

Where was the first roll?

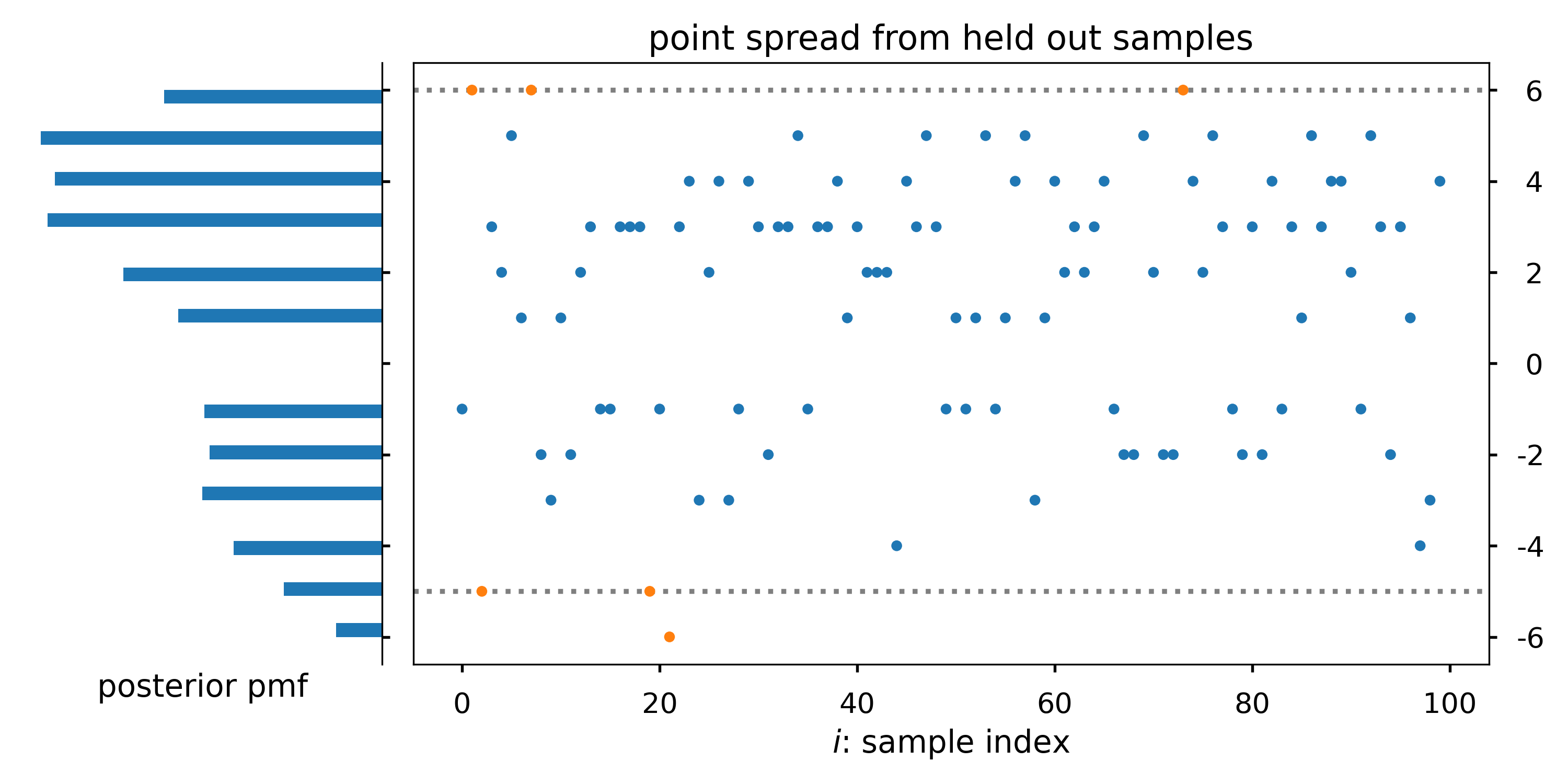

Posterior means

If we play this game many times the posterior mean produces reliable estimates of the position of the first roll

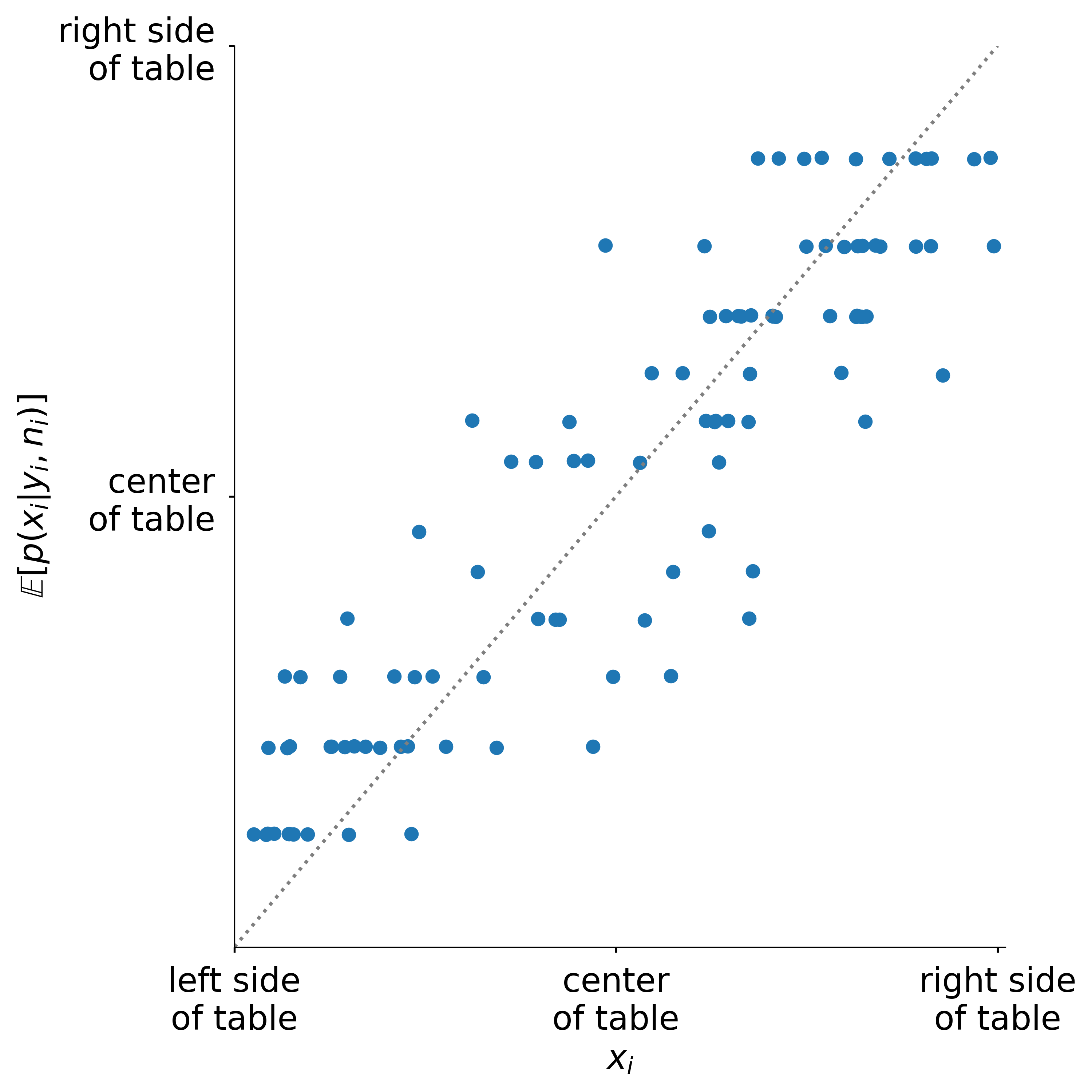

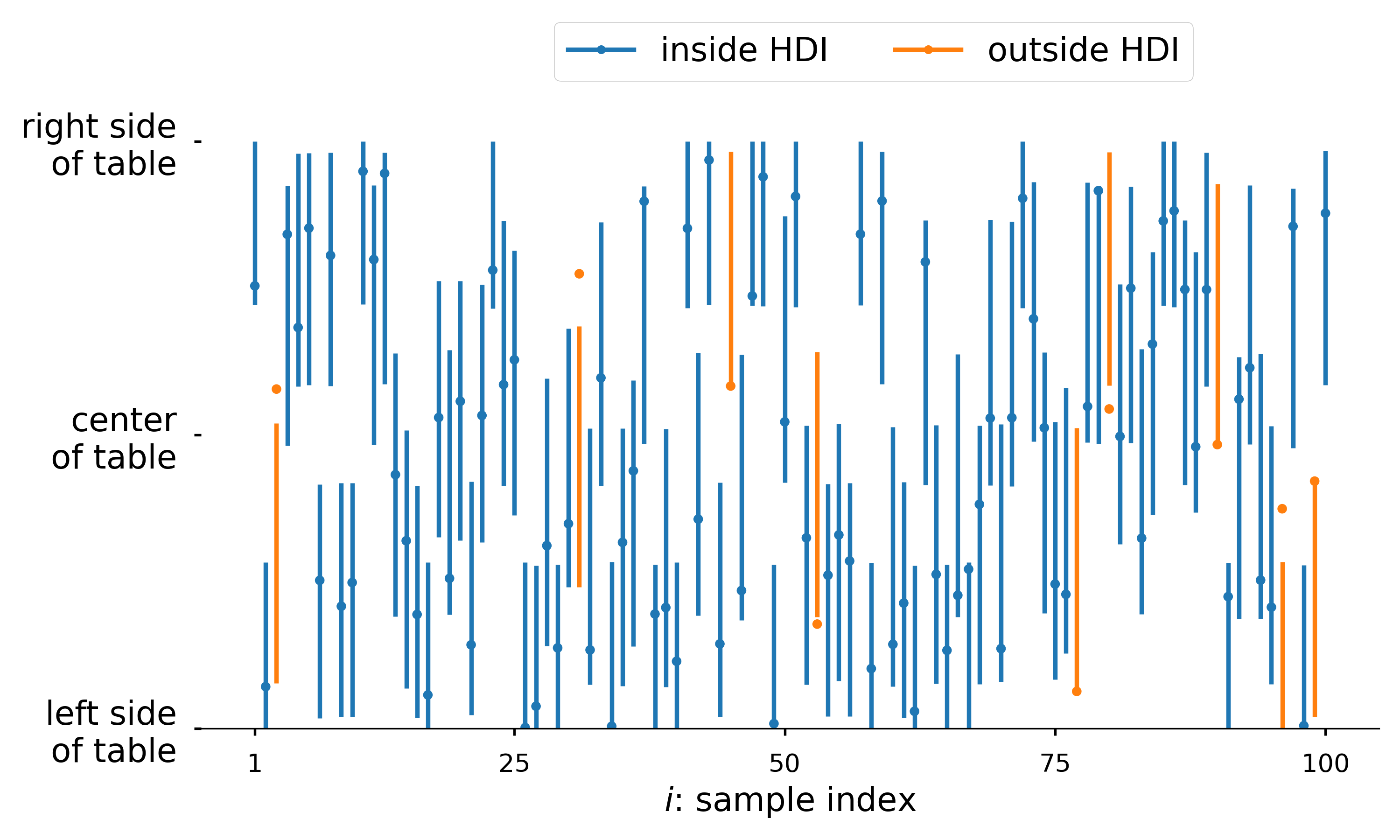

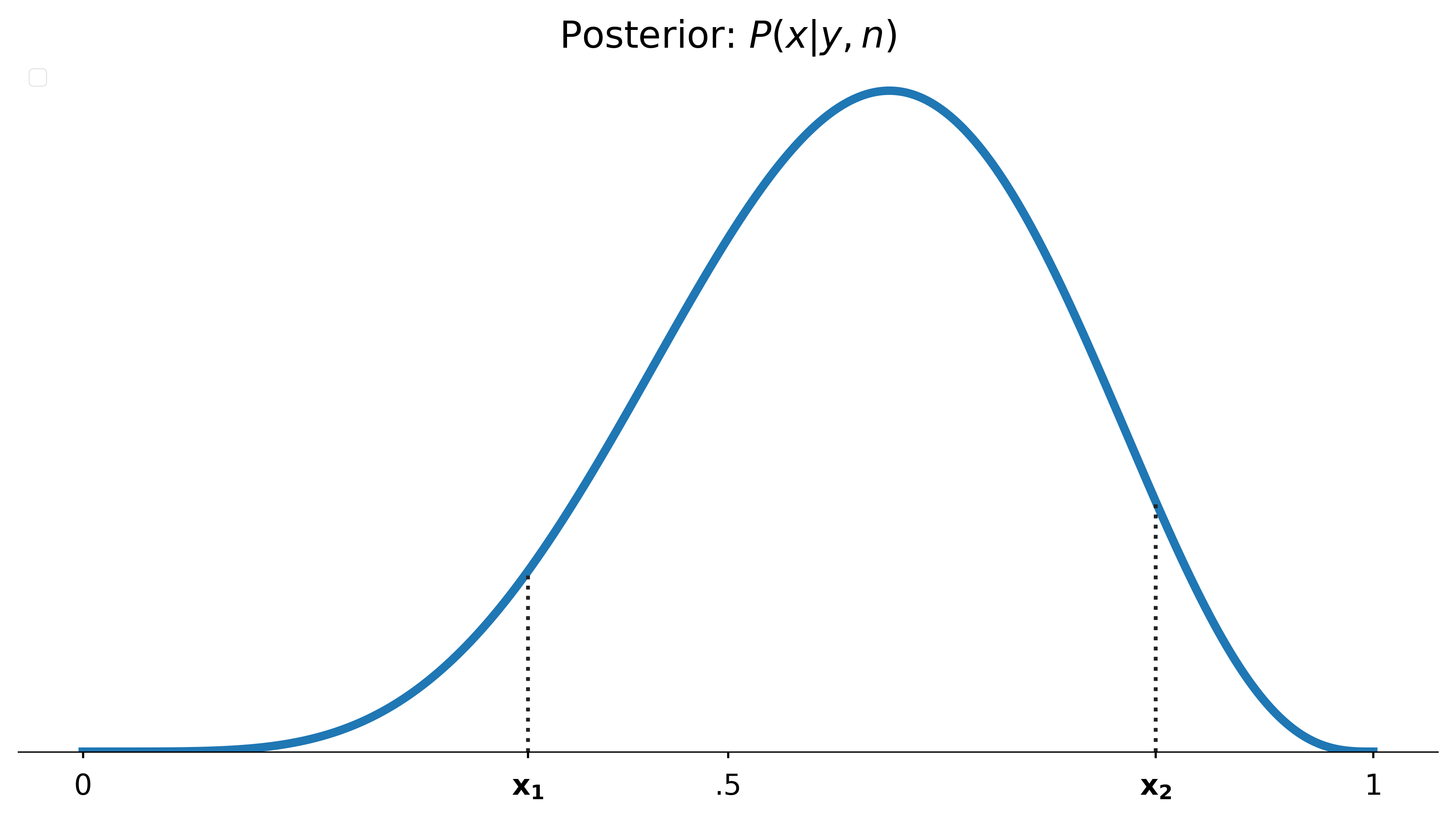

Posterior intervals

The 90% HDI of our posterior contains x_{i} ~90% of the time as expected

Enter HMC

import pymc as pm

alice, bob = 5, 3

with pm.Model() as model:

x = pm.Uniform('x', 0, 1)

likelihood = pm.Binomial('likelihood',

p=x,

n=alice+bob,

observed=alice)

idata = pm.sample()

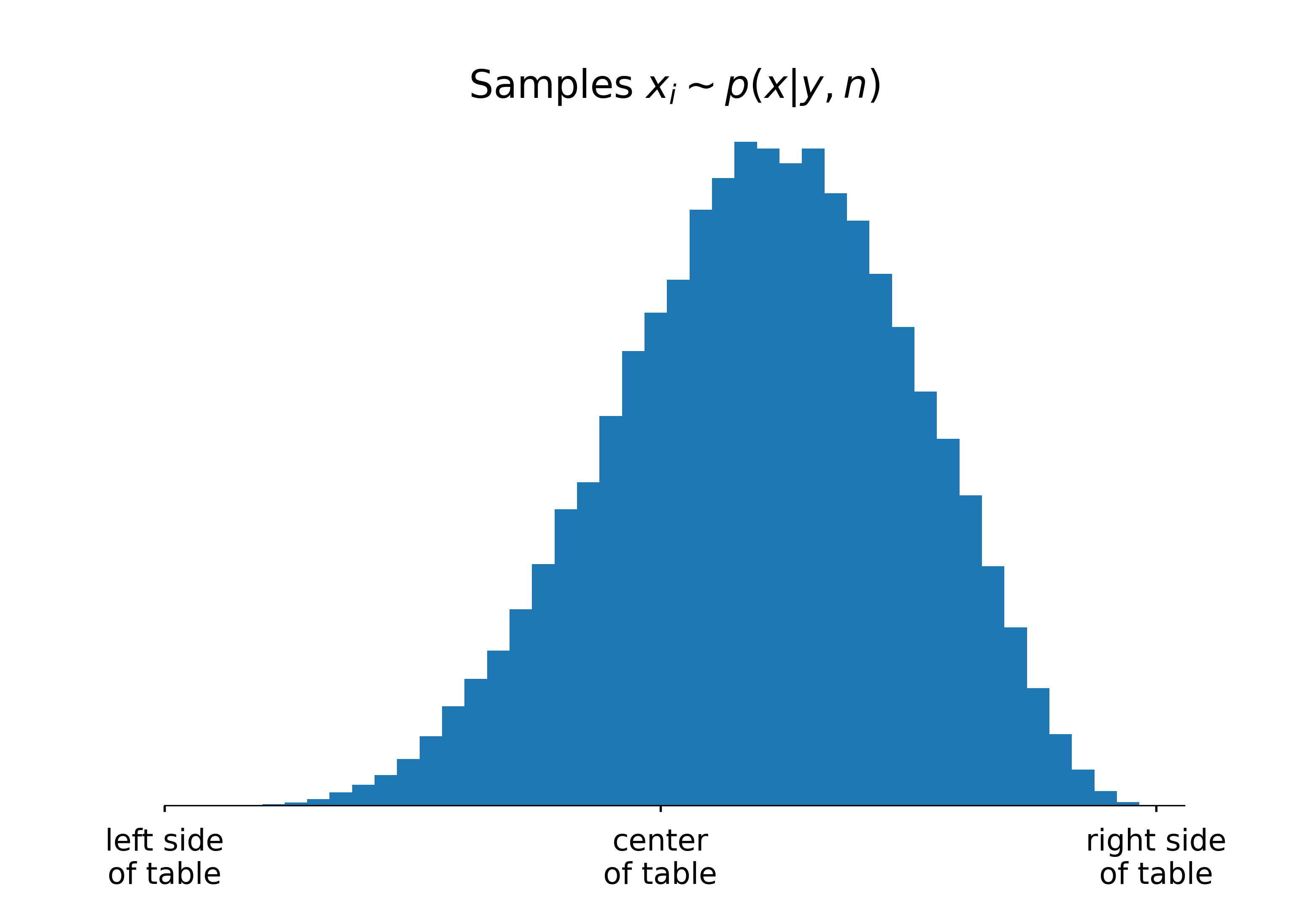

plt.hist(idata.posterior.x)Enter HMC

import pymc as pm

alice, bob = 5, 3

with pm.Model() as model:

x = pm.Uniform('x', 0, 1)

likelihood = pm.Binomial('likelihood',

p=x,

n=alice+bob,

observed=alice)

idata = pm.sample()

# ↓↓↓ approximate the integration ↓↓↓

np.power(1-idata.posterior.x, 3).mean()Random variables in, random variables out

We also expect reliable long term behavior from the posterior predictive distributions. Thus, simulations of, e.g., point spread should exhibit these properties

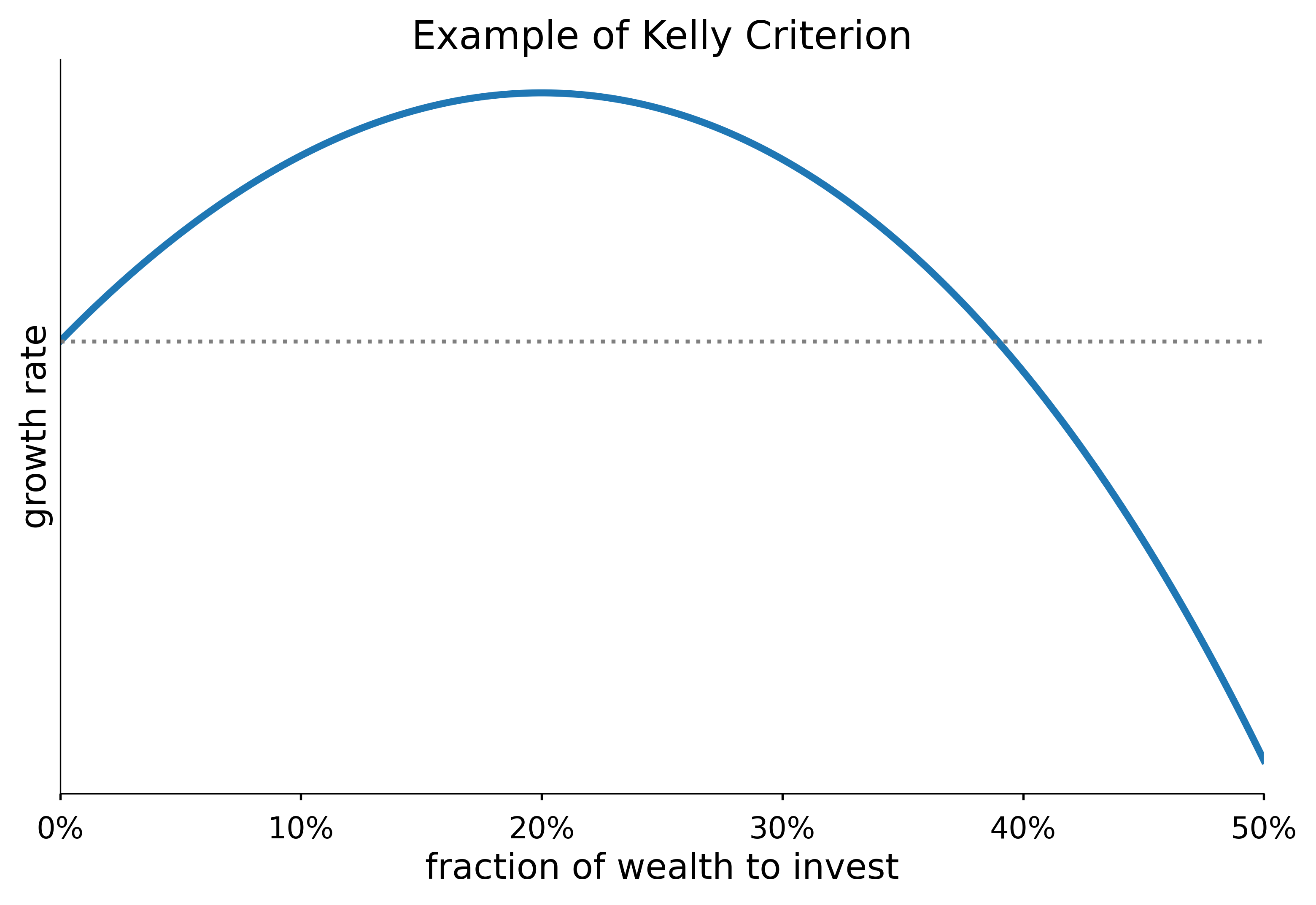

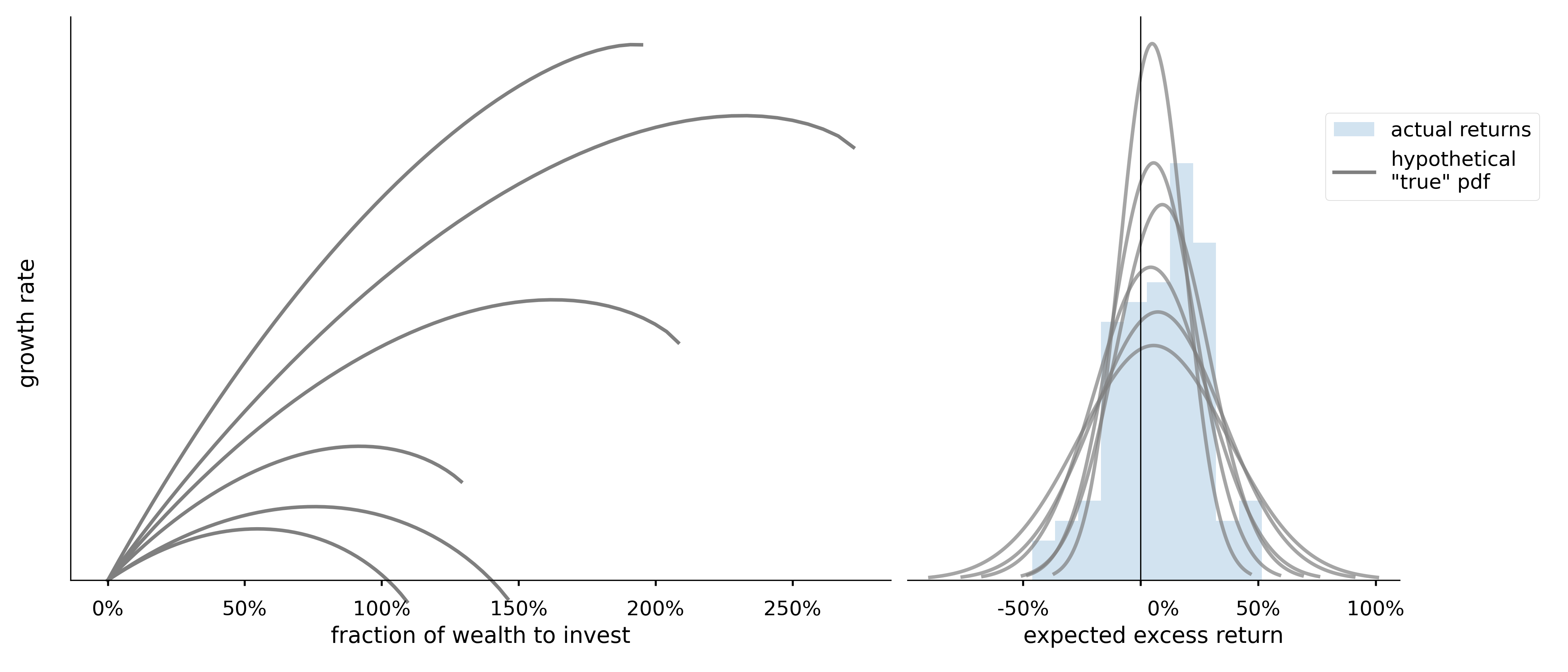

Properties of the Kelly Criterion

Properties of the Kelly Criterion include: a global maximum, a point of diminishing returns and “greed” that produces inevitable ruin.

Ed Thorp and the Kelly criterion

What if we want to apply the Kelly criterion to a “continuous gambling game”, such as the stock market?

Thorp’s conclusion: invest heavily

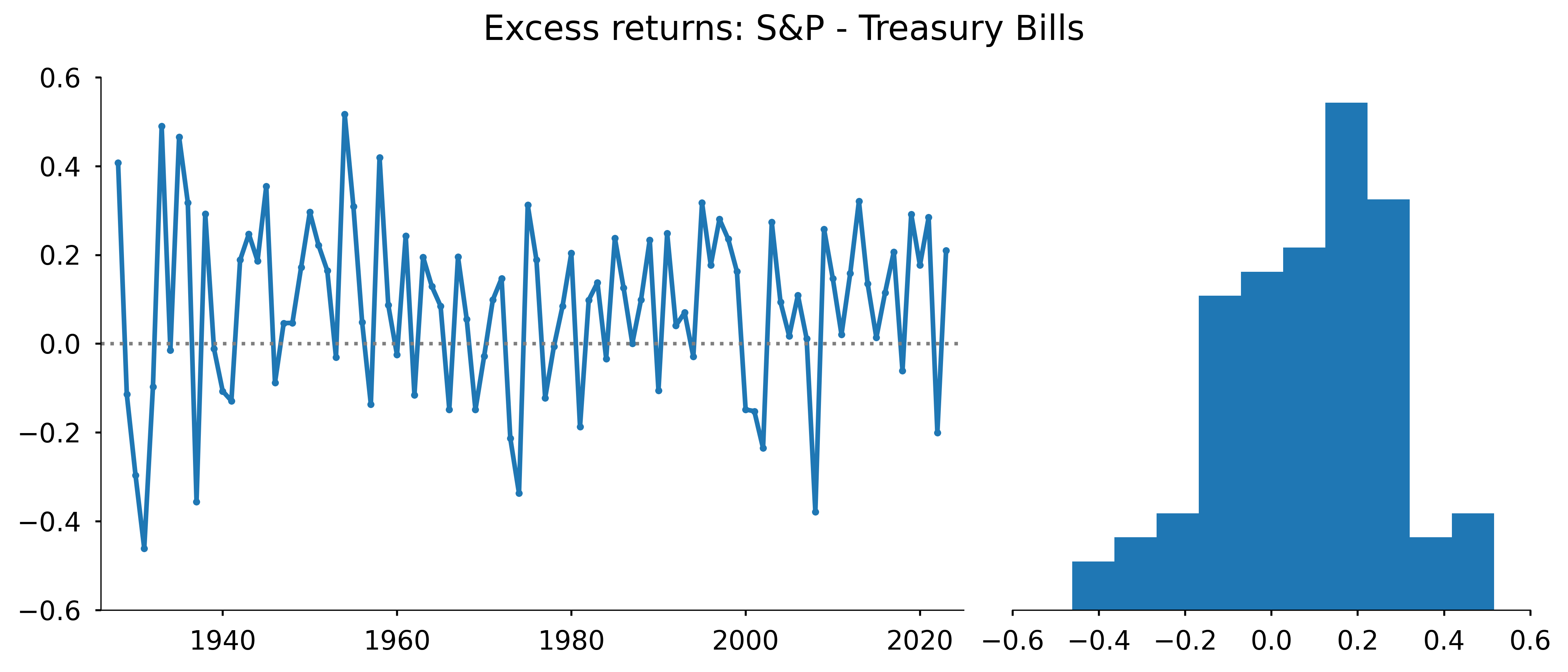

What is the true data generating distribution?

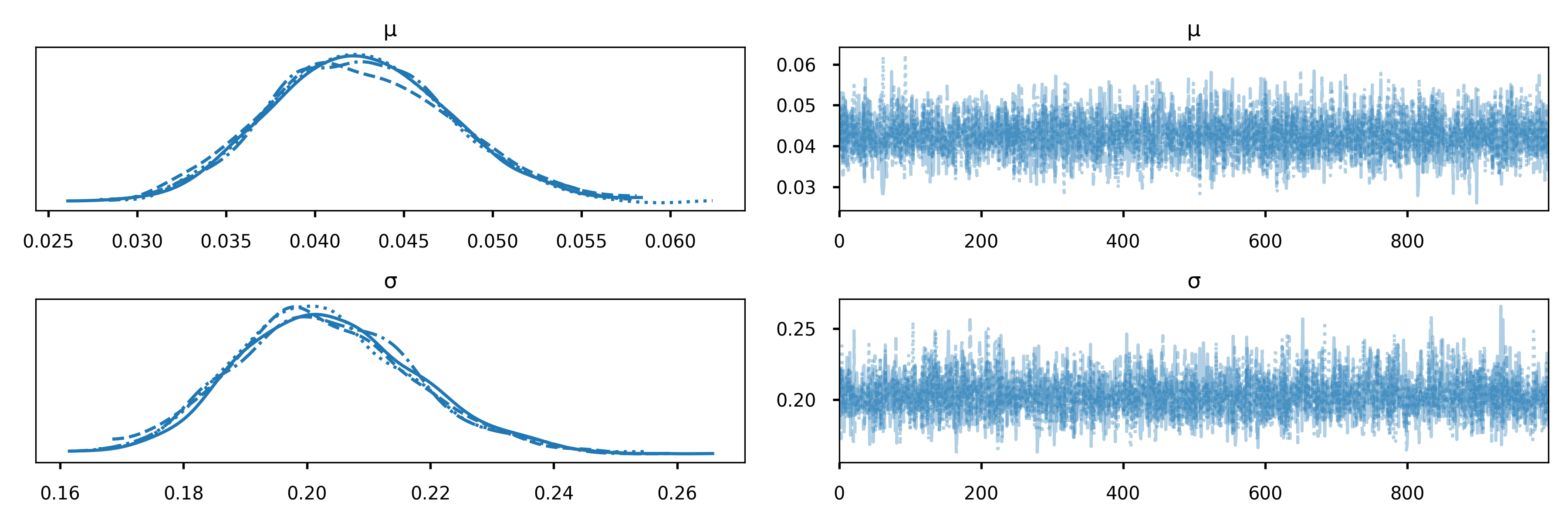

Code

import pymc as pm

with pm.Model() as model:

μ = pm.Gamma('μ', mu=.04, sigma=.005)

σ = pm.Gamma('σ', mu=.2, sigma=.05)

likelihood = pm.Normal('likelihood', mu=μ, sigma=σ, observed=r)

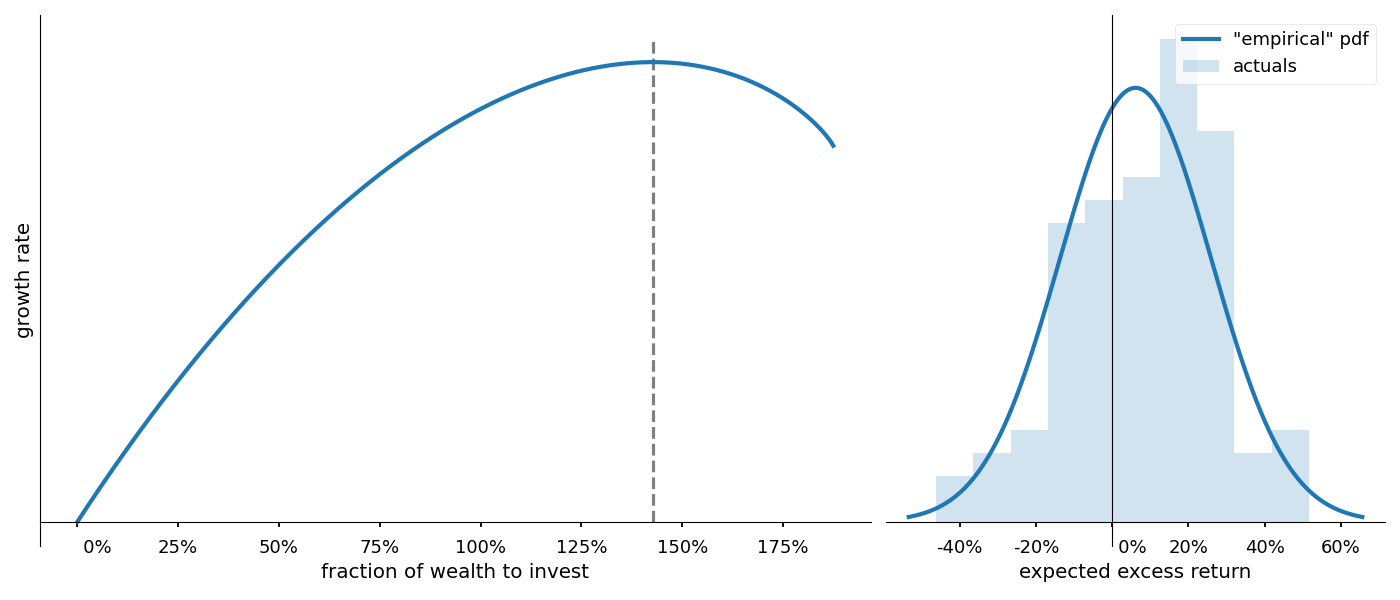

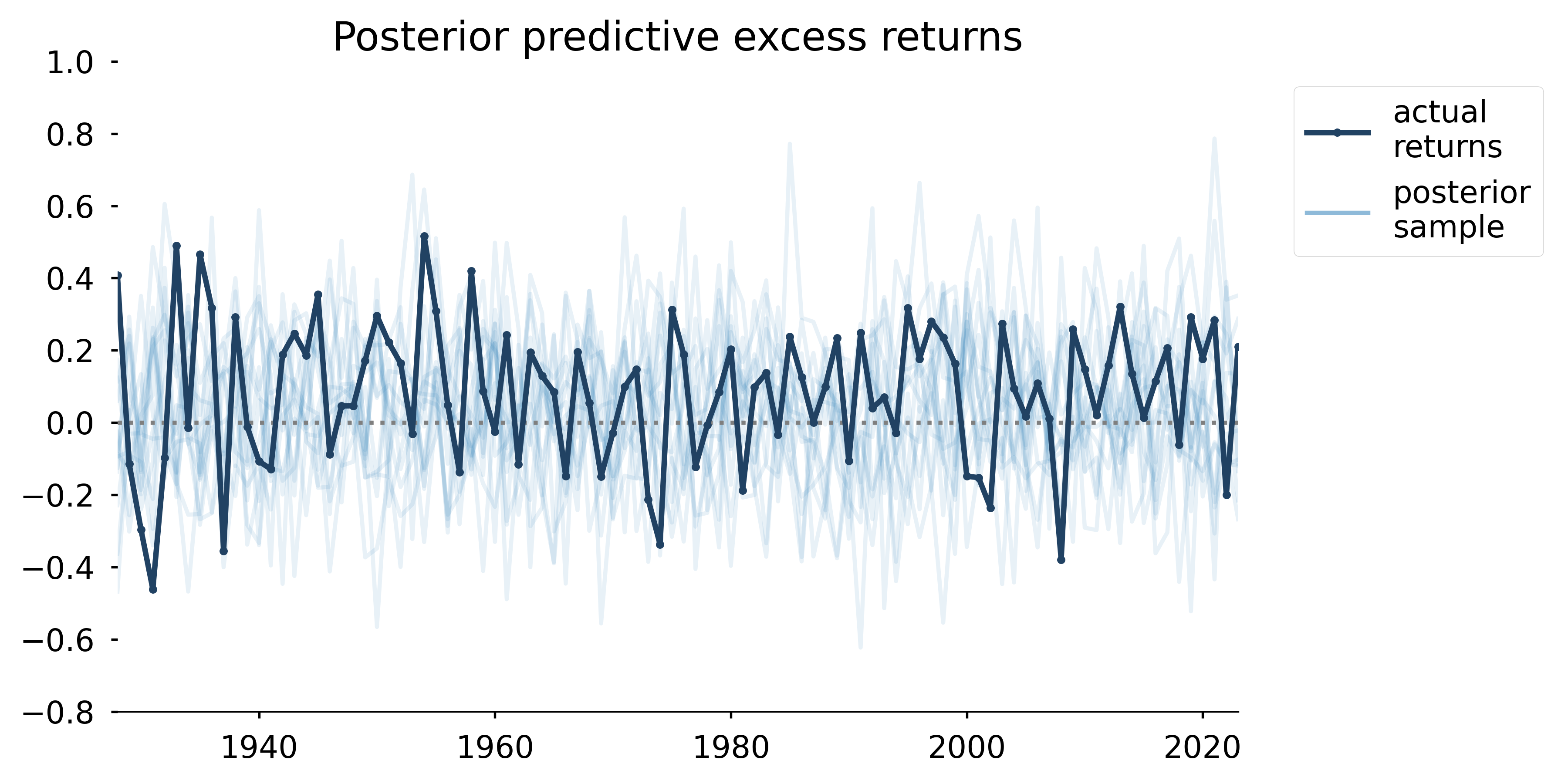

Posterior predictive samples

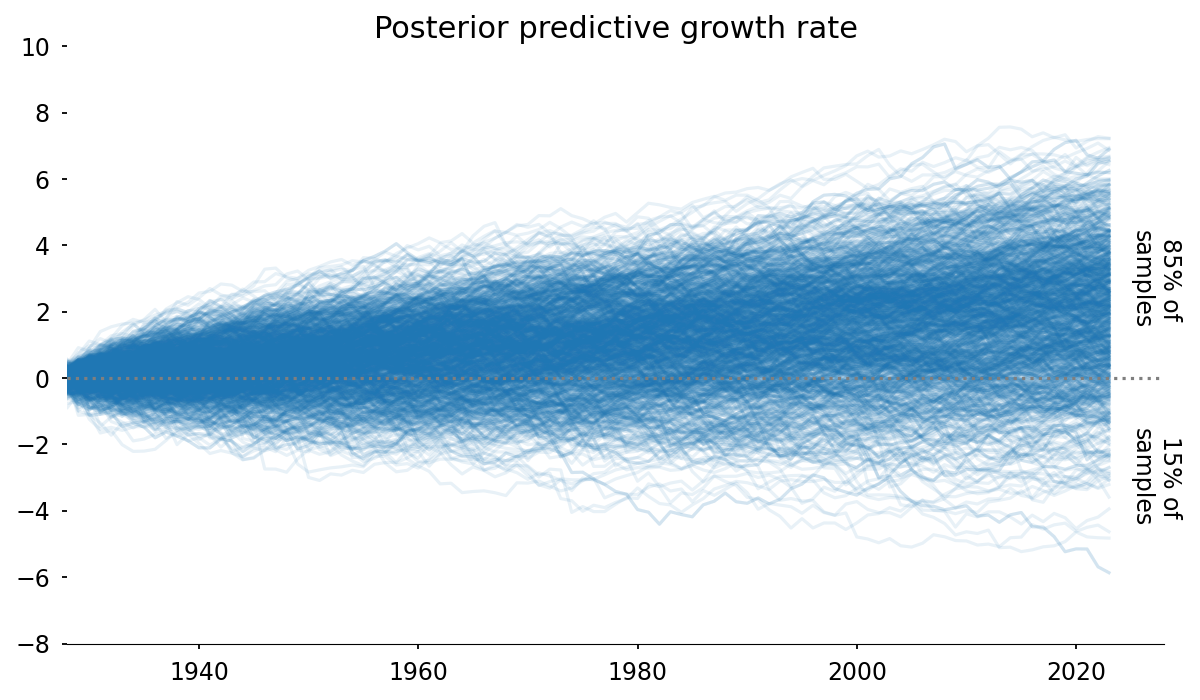

Posterior predictive growth rate

Not only can we extract the usual summary statistics from the posterior predictive, but we can ask questions like, “how often do we expect this strategy to produce a loss after a 100 year investment period?”

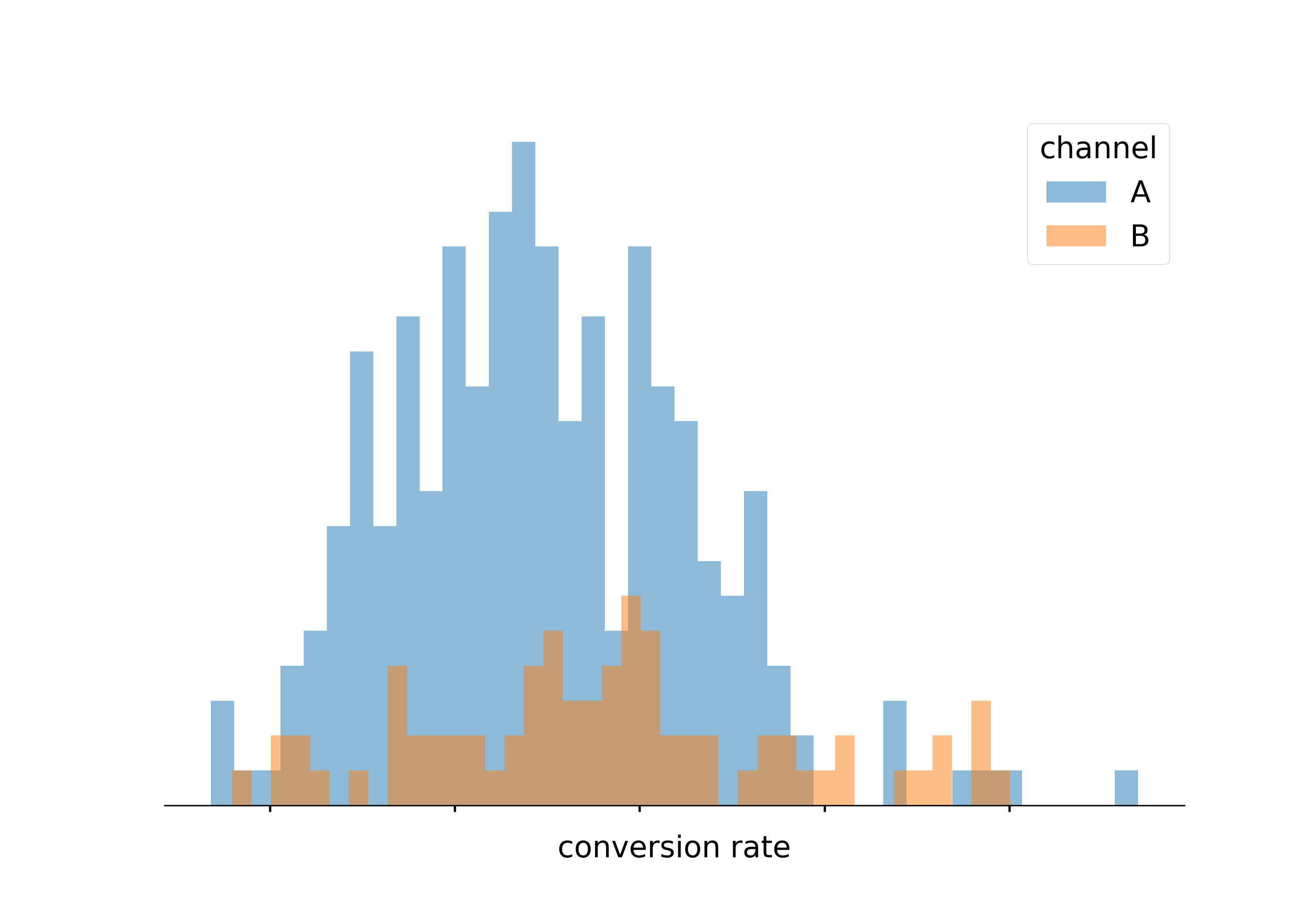

Imagine: these were conversion rates

Imagine: these were conversion rates

Resist the temptation

Similar to point-spread

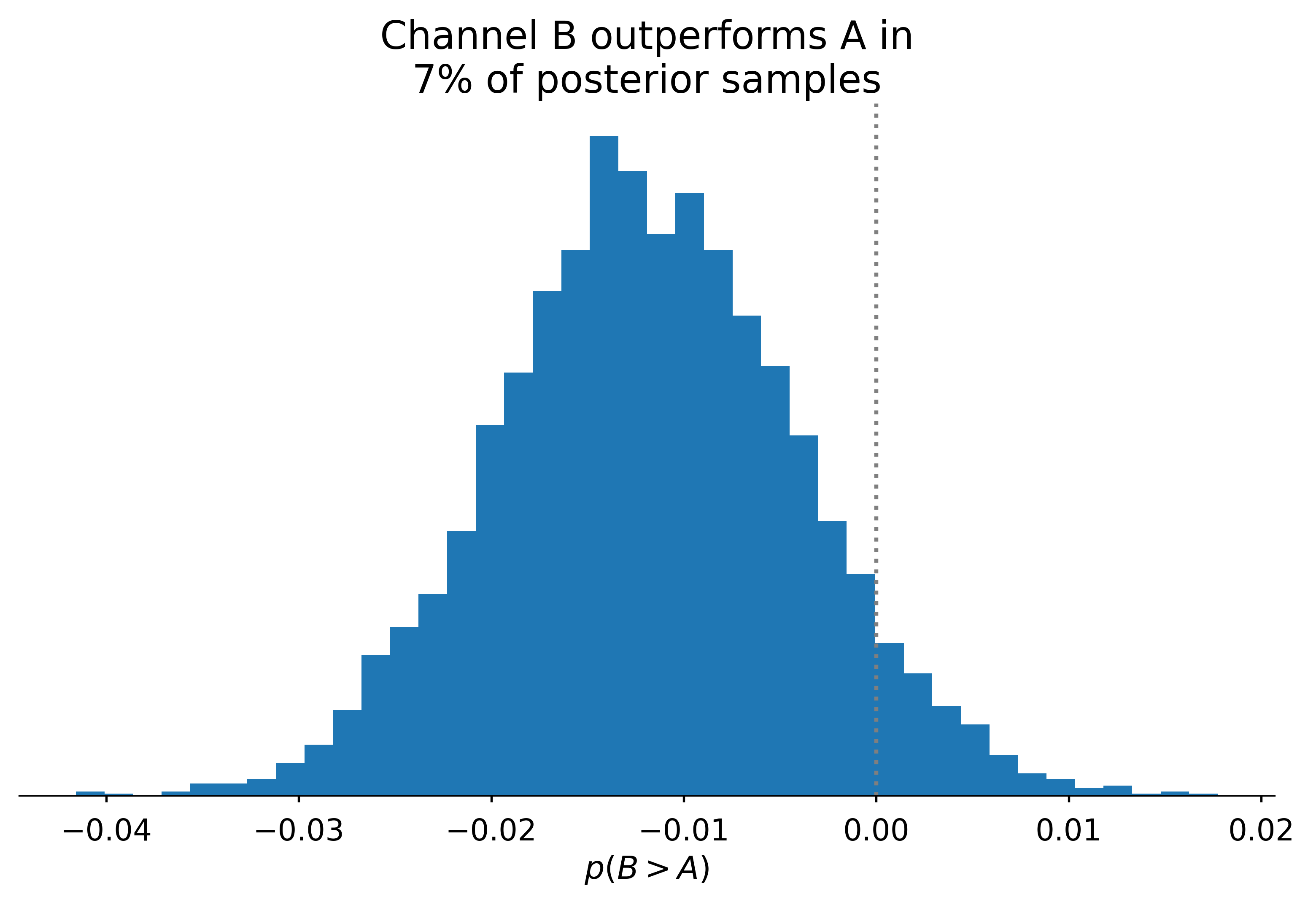

We could consider the probability that one “channel” will outperform another: i.e. p(c_{1} < c_{2})

Comparison

with pm.Model() as model:

θ = pm.Beta('θ', 1, 1, size=2)

pm.Binomial(

'y1', p=θ[0], n=n1, observed=y1

)

pm.Binomial(

'y2', p=θ[1], n=n2, observed=y2

)

idata = pm.sample()

θ_post = idata.posterior.θ

(θ_post[..., 1] > θ_post[..., 0]).mean()Thompson sampling

Thompson sampling allows for “live” A/B testing, where action A is taken according to the probability that A > B.

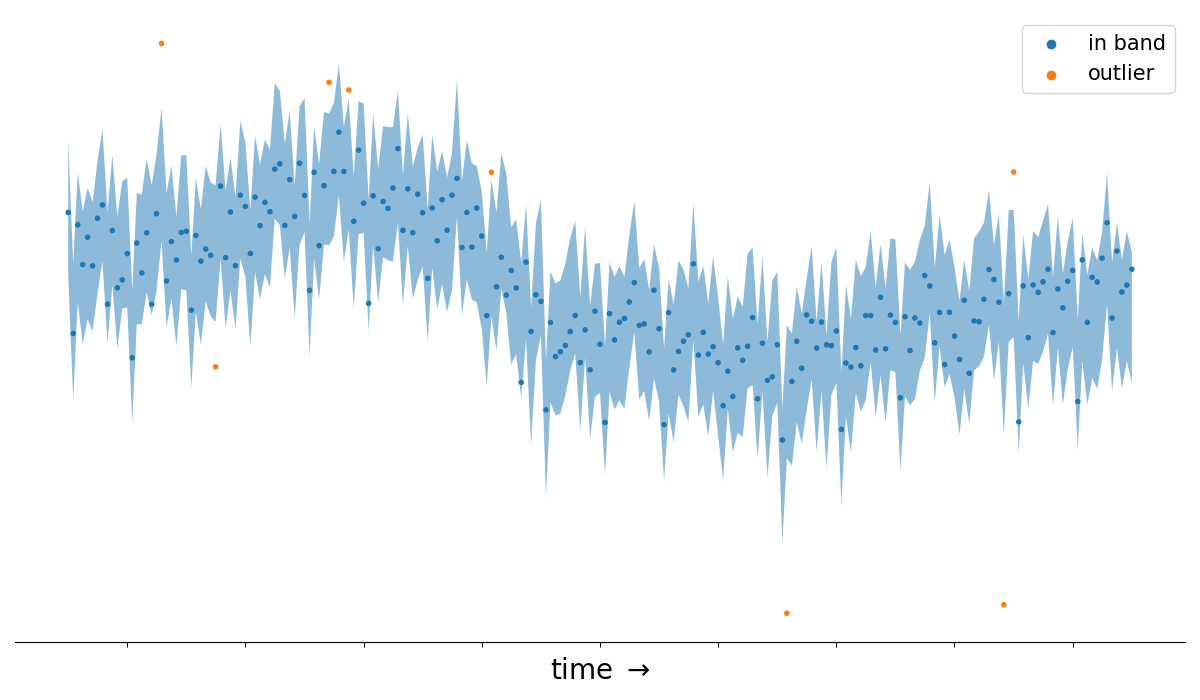

Anomaly detection

These properties also hold for more complex generative models such time series forecasts with trend and seasonal components.

Husband and Father

Philly data scientist

wrote a haiku once